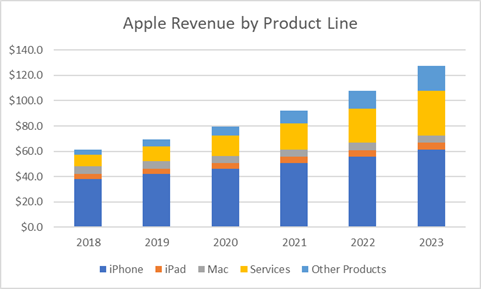

In Q3, the products segment’s gross profit margin decreased 152 basis points year over year to 34.5%, and the services segment’s gross profit margin climbed 169 basis points to finish at 71.5%. So its services segment is not only growing much faster, but it’s also a much more profitable business. It’s clear that Apple could be a much more profitable company by the end of the decade, as its services segment continues to outpace its products category in top-line growth and profitability.

Let’s estimate that the products segment can expand at a compound annual growth rate (CAGR) of 3% through fiscal 2030 from 2021 to $388 billion, and its services segment can rise at a CAGR of 18% to $304 billion. That would bring Apple’s total sales in fiscal 2030 to $692 billion, which is slightly above analysts’ forecasts of $676 billion, according to data from S&P Global Market Intelligence. To boot, the products segment would represent just 56% of revenue, versus 76% in the latest quarter, and its services category would make up 44% of sales, quite the uptick from 24% in Q3. No one knows exactly how the situation will pan out, but based on recent business trends, it’s reasonable to assume that Apple’s services segment will easily outrun its products segment in growth through the end of the decade.

Regardless of exact estimates, I think it’s safe to say that Apple’s future will be determined largely by its services segment, not its hardware products. So investors should keep a close eye on the performance of the services category. It has important implications in regards to Apple’s long-term success, and it’s vital that the segment continue to succeed if the tech giant wants to sustain meaningful growth.

Should investors pounce on Apple stock?

With its one-of-a-kind brand and its $48.2 billion in cash and marketable securities, I’m confident that Apple’s services segment will thrive in the long run. If you already own Apple stock, hold it forever. If you’re looking to start a position or accumulate more shares, I’d wait for the time being. The stock currently trades at 26 times earnings, above its five-year mean of 23.1. I’d suggest that investors wait until its price-to-earnings multiple falls below its historical average.

Apple is a tremendous company, but identifying a good business is only one part of being a great investor. The other part is determining when to buy. In the iPhone maker’s case, now is not the time. Be patient, though — the right moment always comes.